Physical address:

128 City Road, EC1V 2NX, London,UK

Hiring the wrong builder is one of the most expensive mistakes a UK homeowner can make. If you have searched for how to vet a builder UK, this is the guide you need.

Why Lead-Generation Platforms Are Not the Safety Net They Claim to Be

Checkatrade, MyBuilder, Rated People — these platforms have spent millions convincing homeowners that their badge equals protection. The reality is less reassuring. Any sole trader can sign up, pay a monthly subscription, and start collecting reviews. The vetting process amounts to a basic identity check and a credit search. There is no requirement to hold public liability insurance, no verification that trade body memberships are current, and no mechanism to confirm that a five-star review was left by a genuine customer for genuine work.

We have seen the same company operate under multiple listings after a name change, laundering a poor reputation with each rebrand. Reviews can be gamed: a builder with a handful of jobs can ask friends and family to fill out feedback forms, and nobody checks. Platforms profit from contractor subscriptions, creating a conflict of interest — removing a trader costs them revenue. If a contractor takes your money and disappears, the platform’s own terms make clear that its liability is effectively zero. Appearing on Checkatrade is not a credential; it is an advert. The responsibility for due diligence rests with you as the homeowner.

Tip: Treat any review platform listing as a starting point for finding candidates, not as proof they are trustworthy. Your vetting process begins — not ends — when you find a name you want to investigate further.

We once assessed a remedial job where the homeowner had paid over £14,000 to a Checkatrade-listed contractor for a loft conversion. The contractor vanished before installing the staircase or completing the Building Regulations sign-off. When the homeowner raised a dispute, they were told the platform could not compel the trader to return funds. There was no insurance backstop and no trade body to escalate to — a completely avoidable outcome with proper vetting in place.

The Essential Checks Before You Hire Any Builder

Proper vetting takes an hour or two. Compare that to the months of stress and thousands of pounds lost when it goes wrong. Here is what to check — in full, before you sign anything.

- Companies House registration: Search the builder’s legal trading name at gov.uk/get-information-about-a-company. Check the company is active and the registered address matches what they gave you. Sole traders do not need to register, but a limited company absolutely must. If they claim to be limited and do not appear, walk away.

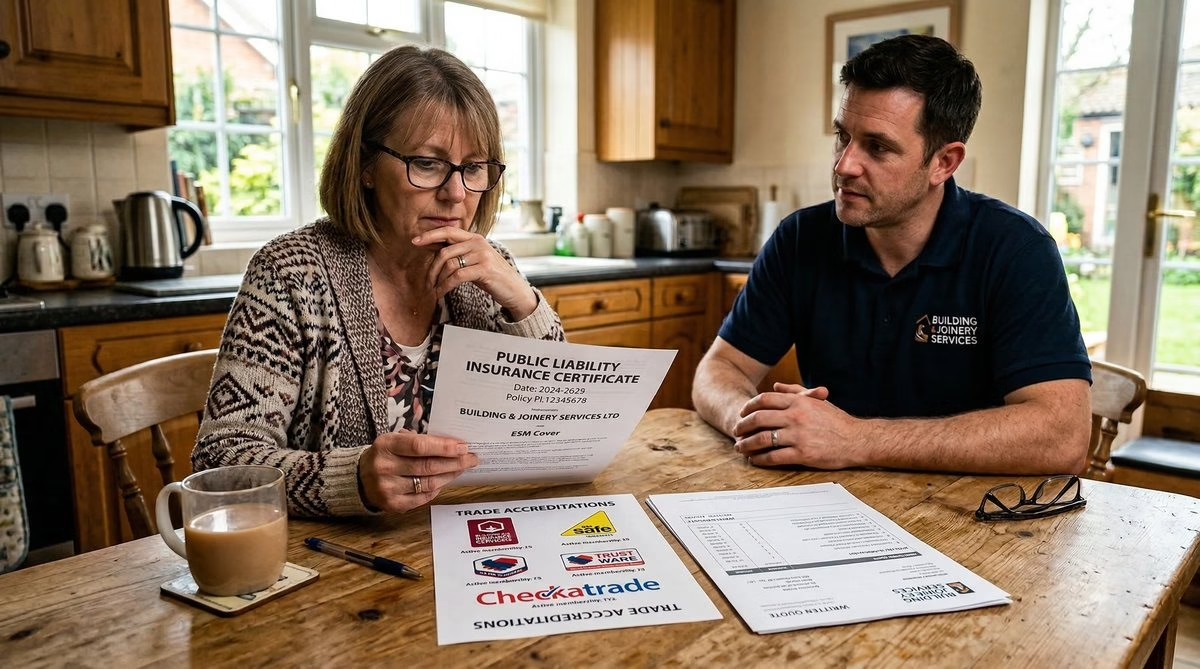

- Public liability insurance certificate: Ask for the actual certificate. It should show a minimum of £1 million cover (£2–£5 million for structural work), the expiry date, and the exact trading name. Call the insurer to confirm the policy is live before work begins.

- Trade body membership: The Federation of Master Builders (FMB), TrustMark, and the NHBC are the three most credible in residential construction. FMB members have been independently inspected. TrustMark is government-endorsed. NHBC is relevant for new builds and major extensions. Each has an online register — search it yourself, as memberships lapse and logos stay on websites long after.

- VAT registration: Any contractor turning over more than £90,000 per year must be VAT-registered. A builder doing large projects who cannot explain the absence of VAT registration is a warning sign.

- Contactable references: Ask for two or three examples of similar jobs completed in the last 18 months with the homeowner’s contact details. Then call. Ask: did it finish on time, did the final cost match the quote, would they hire again? A contractor who hesitates to provide references is telling you something important.

We always tell clients: a reputable builder expects these questions and will have the answers ready without hesitation. If met with irritation or deflection, that reaction itself is a vetting result.

Deposit Rules, Payment Schedules, and Protecting Your Money

The moment your money leaves your account it becomes much harder to recover. Getting the payment structure right before work starts is one of the most effective protections available to you.

The widely accepted rule for deposits is no more than 10 to 15 per cent upfront, or the verified cost of materials ordered for your job — whichever is lower. If a builder asks for 30 or 40 per cent before work begins, decline. The only legitimate reason for a large upfront payment is materials that cannot be procured on short notice, and the builder should provide invoices.

Beyond the deposit, all further payments should be tied to clearly defined milestones in a written schedule. Milestones might include: groundwork complete, first fix carpentry complete, plastering complete, second fix complete, snagging resolved and sign-off received. Each payment should be released only once you have inspected the work and are satisfied. Always pay behind the work, never ahead of it.

- Never pay in cash: Bank transfers create a paper trail. Cash payments give you no evidence of what was paid or why — and make recovery through the courts substantially harder.

- Avoid large lump sums: Break payments into smaller tranches aligned to progress. A contractor who objects to milestone-based payments should be asked why.

- Use a credit card for the deposit where possible: Payments over £100 by credit card attract Section 75 Consumer Credit Act protection, giving you a potential chargeback route if the contractor fails to deliver.

We recently assessed a remedial job where a homeowner had paid 60 per cent upfront — around £22,000 — to a contractor who stopped attending site after three weeks, citing material shortages. There were no shortages. A milestone payment schedule would have capped the exposure at £3,500 at that stage of the job.

What a Proper Written Quote Must Include

A verbal estimate is not a quote. A rough figure scribbled on paper is not a quote. A proper written quote is a document you could present in court, because in a dispute, that is precisely what it becomes. Getting this right before work begins is far easier than reconstructing what was agreed after a relationship has broken down.

At minimum, a written quote for any significant building work should contain:

- Itemised scope of works: Every task broken down individually — demolition, groundwork, brickwork, roofing, first fix, second fix, finishes. Not “full kitchen extension” as a single line item.

- Materials specification: Brand, grade, and specification of key materials. Bricks — which brick, which bond? Insulation — which product, what U-value? Roofing membrane — which brand? Vague materials specs allow a contractor to substitute cheap alternatives and claim they met the brief.

- Start and completion dates: With a clear mechanism for extension due to weather or unforeseen structural issues — but with defined outer limits. Open-ended timelines are a recipe for a project that drags on indefinitely while the contractor juggles other sites.

- Payment schedule: Tied explicitly to milestones, with amounts and trigger conditions stated clearly for each stage.

- Variation process: Any additional work should require a written variation order signed by both parties before it is carried out. Without this clause, you have no protection against a final invoice that bears no resemblance to the original quote.

- Waste disposal: Who is responsible for skip hire and disposal of materials? Left unspecified, this can become a source of unexpected cost and argument.

Tip: If a builder says they do not use written contracts because “we work on trust,” take that as a reason not to trust them. Reputable contractors use written agreements precisely because they make expectations clear for both sides.

Red Flags That Should Stop You Hiring a Builder

Some warning signs are ambiguous; these are not. These are the ones we consider non-negotiable — if you encounter any of them, walk away regardless of how competitive the price appears to be.

- Cash only: Any insistence on cash payment — whether framed as a “discount for cash” or as the only option — should end the conversation immediately. It signals unregistered work, no paper trail, and no recourse if something goes wrong.

- No written quote: If a builder will not commit their scope and price to paper, they are preserving their ability to charge more than you agreed. This is not a misunderstanding — it is a deliberate business model that benefits only them.

- Pressure to start immediately: “I’ve got a gap next Monday — you need to decide now.” Legitimate contractors are busy, but they do not manufacture urgency to bypass your due diligence. This tactic is designed specifically to stop you doing the checks described in this guide.

- No fixed business address: A mobile number and a van is not enough. A contractor of any meaningful scale should have a registered address, a contact number, and a business email. Absence of these makes them very difficult to pursue legally if things go wrong.

- Suspiciously low quotes: If one quote is 40 per cent lower than the others, the builder either plans to cut corners on materials and labour, or intends to escalate the price substantially once work has started and you are too committed to leave. Either way, the outcome is costly.

- No interest in Building Regulations: For notifiable work — extensions, structural alterations, electrical work, and certain window replacements — Building Regulations approval is a legal requirement. A builder who dismisses this exposes you to enforcement action, unsafe work, and complications when you come to sell.

How Fixiz Helps You Find and Work With the Right Builder

At Fixiz, we have built our approach specifically around the problems described above. We do not operate as a lead-generation directory. Every contractor we work with has been vetted directly by our team: insurance certificates checked against the issuing insurer, trade body memberships confirmed on live registers, and references spoken to before any contractor appears on our platform.

We also support clients through the project management process — helping scope works correctly before a single quote is requested, reviewing quotes when they arrive, and flagging anything that does not reflect industry-standard pricing or practice. Over the years we have reviewed hundreds of quotes from London homeowners. A significant proportion contain vague scope descriptions, missing materials specifications, or payment structures that heavily favour the contractor — signs of a contract that will not protect you if something goes wrong.

We also help clients who are mid-project and concerned that things are drifting — costs creeping, timelines slipping, a contractor who has become evasive. An independent view of where the project stands, what has been paid, and what recourse is available can be invaluable in those circumstances. We have helped homeowners recover deposits, get stalled work restarted by a replacement contractor, and navigate the small claims process from start to finish.

When clients come to us after a contractor relationship has broken down, the first question we ask is always the same: what was in the written agreement? In most cases, the honest answer is nothing. That is where disputes begin — and where good preparation would have either prevented the problem entirely or made the path to resolution far clearer. We work with homeowners across London and the South East on projects of every size — whether you are still choosing a builder, mid-build and concerned, or already dealing with an aftermath.

What to Do If Things Go Wrong

Even with thorough vetting, disputes happen. Knowing the correct escalation path before you need it means you are less likely to panic and far more likely to recover your money or get the work finished properly. Here is the sequence to follow.

- Start with written communication: As soon as a problem emerges, put everything in writing. State the issue clearly, reference the relevant clause in your contract, and give a reasonable deadline — seven to fourteen days — for the contractor to respond or remedy the problem.

- Letter before action: If that fails, send a formal letter before action stating you intend to issue a small claims court claim if the issue is not resolved within fourteen days. This step is required before filing and often prompts resolution without court.

- Small claims court: For disputes up to £10,000 in England and Wales, the small claims track is accessible without a solicitor. File online at gov.uk and keep all invoices, bank statements, photographs, and written correspondence as your evidence bundle.

- TrustMark dispute resolution: If your contractor holds TrustMark registration, TrustMark operates a free dispute resolution service. They can investigate complaints and remove traders from the scheme in cases of serious misconduct.

- FMB arbitration: FMB members can be referred to the FMB’s free conciliation service and independent adjudication — often faster and cheaper than court for disputes between £5,000 and £50,000.

- Trading Standards: For fraud, misrepresentation, or repeated rogue trading, report your case via the Citizens Advice consumer helpline. Individual complaints contribute to enforcement action against serial offenders.

Tip: Never withhold payment without a documented reason, and never abandon the site yourself during an active dispute. Both can complicate your legal position. Continue communicating in writing, keep records of every interaction, and let the dispute resolution process work at its own pace.

Frequently Asked Questions

Is a builder on Checkatrade automatically vetted and insured?

No. A Checkatrade listing confirms the trader has paid for a subscription and passed a basic identity check. It does not confirm current public liability insurance, active trade body memberships, or genuine reviews. Independent verification remains your responsibility.

How much deposit is reasonable to pay a builder before work starts?

No more than 10 to 15 per cent of the total contract value, or the confirmed cost of materials that must be ordered for your job. Any request significantly above this should be treated as a warning sign.

What trade body memberships should I look for when vetting a builder?

FMB membership requires an independent inspection and is a strong signal of quality. TrustMark is government-endorsed and covers a wide range of trades. NHBC is relevant for new builds and major extensions. Always verify directly on the relevant body’s website.

Do I need a written contract for small jobs?

For any job above a few hundred pounds, yes. A detailed written quote signed by both parties is sufficient — it records the agreed scope, price, materials, and timeline, and gives you a clear basis for dispute resolution.

What can I do if a builder has disappeared after taking a deposit?

Document all contact attempts in writing. If there is no response, send a letter before action by recorded post to the contractor’s registered or last known address. If that fails, issue a small claims court claim online for up to £10,000. If you paid by credit card, pursue a Section 75 claim with your card issuer. Report to Trading Standards via Citizens Advice regardless.

Ready to move from confusion to construction? Get in touch with Fixiz today for a no-pressure chat about your project and the fastest route to full compliance.